Introduction

In many UK accounting firms, audit delays are often blamed on workload, deadlines, or client complexity.

But as we explored earlier, the real issue runs deeper.

The biggest bottleneck in audit workflows is working papers.

They sit at the centre of every audit yet they are also where the most audit inefficiencies occur.

So the real question is:

What exactly is slowing down working papers and how are modern firms solving it?

Why Working Papers Become a Bottleneck

Working papers are meant to support clarity, structure, and compliance.

But in reality, they often become:

- Disorganised

- Time-consuming

- Difficult to review

- Hard to standardise

This is not because teams lack expertise, it’s because the system around working papers is broken.

The 5 Core Reasons Working Papers Slow Down Audits

- Disconnected Tools and Files

In many firms, working papers live across:

- Excel spreadsheets

- Word documents

- Shared drives

- Email threads

This creates:

- Constant switching between tools

- Lost context

- Time wasted searching for information

Instead of a single workflow, teams deal with fragmentation.

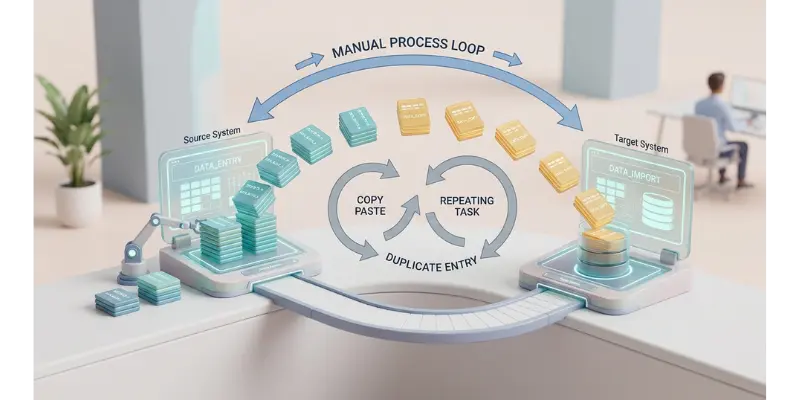

- Manual Data Handling

A large part of working papers still depends on:

- Copy-pasting data

- Manual updates

- Re-entering figures

This leads to:

- Higher risk of errors

- Repetitive work

- Significant time loss

Even small inefficiencies, repeated across audits, create major delays.

- Lack of Real-Time Collaboration

Audit teams rarely work in isolation but their tools often do.

Common challenges include:

- Multiple versions of the same file

- Overwritten changes

- Delayed updates between team members

Collaboration becomes reactive instead of seamless.

- Inefficient Review Workflows

Review is where working papers slow down the most.

Typical issues:

- Comments scattered across emails

- No clear review trail

- Difficulty tracking changes

This results in:

- Rework

- Confusion

- Delayed approvals

- No Standardised Structure

Different team members often structure working papers differently.

This leads to:

- Inconsistent documentation

- Slower reviews

- Increased training time for new staff

Lack of standardisation = lack of efficiency.

The Compounding Effect

Each of these issues may seem small individually.

But together, they create:

- Longer audit cycles

- Increased operational cost

- Frustrated teams

- Reduced capacity for firms

This is why simply “working harder” doesn’t solve the problem.

How Modern Accounting Firms Are Fixing This

Forward-thinking UK firms are not just improving workflows, they are rebuilding them from the ground up.

Here’s what’s changing:

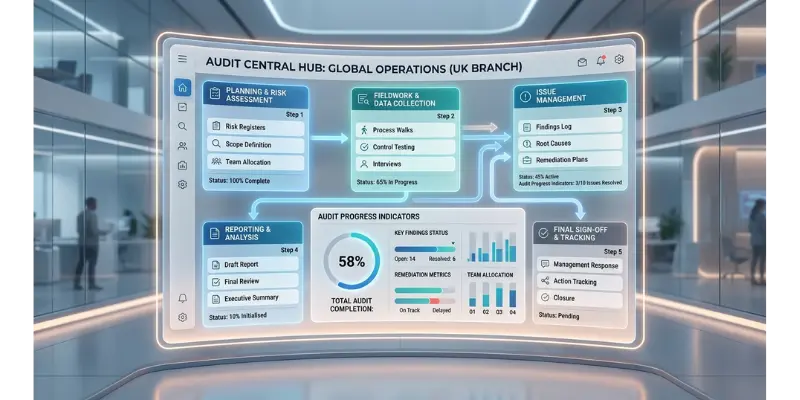

✔️ Centralised Working Paper Systems

Instead of scattered files, everything lives in one place:

- Structured documentation

- Easy navigation

- Complete audit trail

✔️ Automated Data Flow

Manual data handling is being reduced through:

- Integrated data inputs

- Automated updates

- Reduced duplication

✔️ Real-Time Collaboration

Teams can now:

- Work on the same data simultaneously

- Track changes instantly

- Avoid version conflicts

✔️ Structured Review Processes

Modern workflows introduce:

- Clear review stages

- Centralised comments

- Transparent audit trails

✔️ Standardised Templates and Workflows

Firms are adopting:

- Consistent working paper formats

- Predefined structures

- Repeatable processes

Where Technology Fits In

This shift is not just about better discipline and it is also enabled by better tools.

Modern working paper platforms are designed to:

- Eliminate fragmentation

- Improve visibility

- Streamline collaboration

- Reduce manual effort

Instead of forcing teams to adapt to tools like spreadsheets, these systems are built specifically for audit workflows.

A Practical Shift – Not Just a Trend

Many small and mid-sized UK accounting firms are already:

- Moving away from spreadsheet-heavy processes

- Adopting structured working paper systems

- Reducing audit turnaround time

- Increasing team efficiency without increasing headcount

This is not about replacing accountants, it’s about removing the friction around their work.

Conclusion

Working papers should support audits and not slow them down.

But in many firms, outdated processes and disconnected tools have turned them into a major bottleneck.

The firms that are solving this are not doing more work, they are doing smarter work with better systems.

And as audit demands continue to increase, this shift will move from advantage to necessity.